- BeanWealth

- Posts

- 7 Green Flags That Every Investor Must Know

Good Evening! 👋

Welcome to Wealth Wednesday! I have had a few people ask me to do 7 Investing Green Flags after I did the 7 Red Flags Article. You can read that one here!

SPONSORED

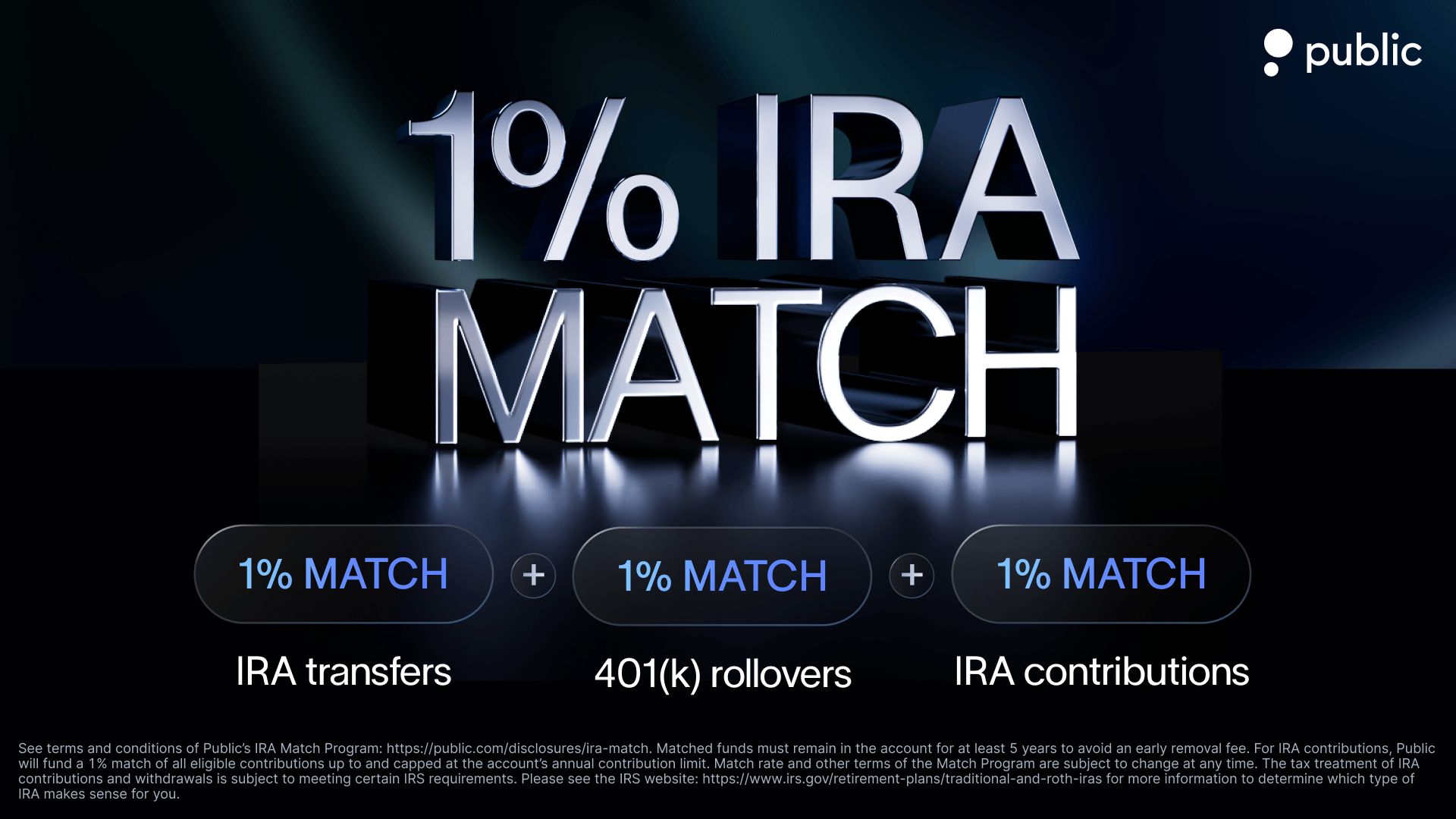

Open Your Roth IRA on Public Today

While most investors let their retirement accounts sit idle, smart investors are supercharging theirs with Public.com’s Roth IRA Triple Play.

Here’s why it’s the best move you can make this year:

✓ 1% match on annual Roth IRA contributions – extra income that doesn’t count toward your IRS limit

✓ 1% match on every 401(k) rollover – easy transfers with our Capitalize partnership

✓ 1% match on IRA transfers – Public even covers transfer fees

✓ Uncapped earning potential – no match limits on rollovers or transfers

Disclosures: Paid endorsement. Brokerage services by Public Investing, member FINRA/SIPC. Investing involves risk. Not an investment recommendation. See terms of IRA Match Program here: public.com/disclosures/ira-match

Dear friends,

Most investors train their eyes to spot danger. They want to know what could go wrong and how to avoid it. That is smart, but the real edge often comes from recognizing the signs of strength.

The truth is, balance sheets and financial statements don’t just hide red flags. They also shine a light on green flags that point to healthy, durable businesses.

When I started out, I spent too much time chasing hype and too little time paying attention to the numbers that revealed a company’s real quality. Over the years, I’ve learned that spotting green flags can be just as important as avoiding red ones.

Today, I want to walk you through seven of the most important green flags I look for when analyzing a company. These signals don’t guarantee success, but they tilt the odds heavily in your favor.

1. Strong Balance Sheet

A healthy balance sheet is one of the clearest signs of strength. It means the company is not overburdened by debt, has enough liquidity to cover short-term needs, and has flexibility to invest when opportunities show up.

Why it’s a green flag:

A company with a strong balance sheet can survive downturns, outlast competitors, and double down when markets get tough. Instead of scrambling to pay lenders, management can focus on growing the business and rewarding shareholders.

Example: Apple

Apple’s massive cash reserves have given it freedom that most companies can only dream of. When economic uncertainty hit in 2020, Apple didn’t slow down. It kept investing, innovating, and even buying back stock. That kind of resilience comes directly from financial strength.

What to look for:

Debt-to-equity ratio under 1: Shows the company isn’t overly reliant on debt.

Current ratio above 1.5: Indicates short-term assets easily cover short-term liabilities.

Growing cash position: Cash in the bank provides a safety net and optionality for acquisitions, dividends, or buybacks.

2. Positive Free Cash Flow

Free cash flow is the lifeblood of a business. It’s the cash left over after paying expenses and making the necessary investments to keep the business running. Companies that consistently generate positive free cash flow are in control of their own destiny.

Why it’s a green flag:

Free cash flow gives a company options. It can reinvest in growth, return money to shareholders, or simply build a war chest to seize opportunities when others are forced to retreat. A company with steady free cash flow is less dependent on borrowing and better positioned to handle shocks.

Example: Berkshire Hathaway

Warren Buffett has made free cash flow a cornerstone of Berkshire Hathaway’s strategy. Today the company is sitting on an astonishing $347 billion in cash. That didn’t happen by accident. Berkshire’s businesses throw off enormous cash year after year, allowing Buffett to wait patiently for moments when he can buy great assets at a discount. This cash position isn’t just a buffer, it’s firepower.

What to look for:

Consistently positive FCF: A track record across multiple years and cycles.

FCF margin above 10%: A strong sign the company is turning revenue into real cash.

CapEx well-covered by operating cash flow: Shows the company can fund its future without relying on debt.

3. Consistent Revenue and Earnings Growth

Flashy one-off quarters can make headlines, but true strength shows up in steady, compounding growth. Companies that expand revenue and earnings year after year tend to build durable value for shareholders.

Why it’s a green flag:

Consistent growth shows that demand is steady, the business model is working, and management is executing. Over time, even modest growth rates can compound into extraordinary results for investors.

Example: Costco

Costco is not a company that grows by hype or big promises. Instead, it grows slowly and steadily, powered by its membership model and customer loyalty. Revenue and earnings march higher almost every single year. That discipline and predictability make it one of the most reliable compounders in the market.

What to look for:

5–10 year revenue CAGR: A steady growth rate over a long horizon.

Earnings growth aligned with revenue: Earnings should rise as revenue does, not be propped up by accounting tricks or cost cuts.

Resilience during downturns: Companies that keep growing through recessions show real strength.

4. High Return on Invested Capital (ROIC)

It’s not just about how much money a company makes, but how efficiently it reinvests that money. Return on invested capital measures how well a business takes the profits it generates and puts them back to work.

Why it’s a green flag:

A company with a high ROIC doesn’t need to pour endless amounts of cash into its operations to grow. That means it can expand while still generating excess cash for shareholders. Over time, this efficiency creates compounding wealth.

Example: See’s Candies

Warren Buffett often points to See’s Candies as a textbook case. The business required very little reinvestment to keep running, yet it produced strong returns year after year. That excess cash could then be funneled into other Berkshire Hathaway investments. It’s the kind of capital efficiency Buffett loves.

What to look for:

ROIC consistently above 10–12%: Shows the company creates real value above its cost of capital.

Stable or rising trend: Sustained performance signals management knows how to allocate capital effectively.

Low reinvestment needs: Businesses that generate strong returns without requiring constant capital infusions are rare and valuable.

5. Prudent Capital Allocation

Even the most profitable company can destroy value if management spends money recklessly. Great businesses are run by leaders who think carefully about how to reinvest profits, when to return cash to shareholders, and when to simply sit on the sidelines.

Why it’s a green flag:

Prudent capital allocation protects shareholder value. It means management isn’t chasing flashy acquisitions or wasting money, but instead is focused on compounding returns in the smartest way possible.

Example: Constellation Software

Since 2009, Constellation Software’s stock has returned an incredible 16,044.60%. That success comes from a disciplined playbook of acquiring small, profitable software companies and letting them continue to operate independently. Instead of overpaying for hype, Constellation targets niche businesses with stable cash flows, then reinvests those earnings into more acquisitions. It’s one of the best examples in modern markets of capital allocation done right.

What to look for:

A clear track record: Study past decisions. Have acquisitions added value or destroyed it?

Shareholder-friendly policies: Sustainable buybacks or dividends that don’t compromise growth.

Discipline in execution: Management avoids empire-building and focuses on returns.

6. Strong Competitive Moat

A competitive moat is what protects a company from rivals. It could be a powerful brand, cost advantages, network effects, or switching costs that make it hard for customers to leave. Without a moat, even the best business eventually gets eaten alive by competition.

Why it’s a green flag:

A strong moat preserves margins and market share. It allows a company to keep growing without constantly fighting price wars or losing ground to new entrants. Moats don’t just defend profits, they extend the life of a business’s advantage.

Example: Visa

Visa’s moat is its network. Millions of merchants and billions of consumers worldwide rely on it. Every new cardholder and every new business that accepts Visa makes the network stronger, creating a flywheel effect that is nearly impossible to replicate. That network effect has helped Visa dominate global payments while maintaining high profitability.

What to look for:

Stable or rising margins: A sign the company isn’t under constant pricing pressure.

Market share leadership: The ability to defend or grow its position over time.

Clear barriers to entry: Evidence that competitors struggle to gain traction.

7. Aligned Incentives

When management and shareholders have their interests aligned, everyone rows in the same direction. The clearest sign of this is when executives and founders own meaningful stakes in the business. It ensures they think like owners, not just hired hands.

Why it’s a green flag:

Skin in the game changes behavior. Leaders with real ownership are more likely to make long-term decisions, avoid unnecessary risks, and focus on building durable value. On the other hand, managers who only collect a paycheck might chase short-term wins at the expense of shareholders.

Example: Amazon

Jeff Bezos built Amazon with a founder’s mindset and kept significant ownership throughout its rise. That equity stake tied his personal wealth to the company’s long-term performance, driving a culture of reinvestment and innovation. Investors who partnered with him early benefited from the same alignment that guided his decisions.

What to look for:

Insider ownership: Executives and directors holding a meaningful percentage of shares.

Management buying shares: Voluntary purchases are a strong vote of confidence.

Reasonable compensation: Pay structures that reward performance, not guaranteed bonuses.

Cheers,

SUGGESTIONS

Poll

If you have any questions or feedback or just wanna say hey, simply reply to this email.

See you on Sunday!

Matt Allen

Disclaimer for BeanWealth

BeanWealth is a publisher of financial education and information. We are not an investment advisor and do not provide personalized investment advice or recommendations tailored to any individual's financial situation. The content provided through our website, newsletters, and any other materials is for educational purposes only and should not be construed as financial or investment advice.

All information is provided “as is,” without warranty of any kind. BeanWealth makes no representations or guarantees regarding the accuracy, completeness, or timeliness of the information presented. The opinions and views expressed in our content are those of the author(s) and do not necessarily reflect the views of BeanWealth, its partners, or its affiliates.

Investors should perform their own due diligence and consult with a professional financial advisor before making any investment decisions. None of the information provided herein constitutes a solicitation to buy or sell any securities or financial instruments. Any projections or forecasts mentioned are speculative and subject to risks and uncertainties that could cause actual outcomes to differ.

BeanWealth, its employees, and affiliates may hold positions (long or short) in the securities or companies mentioned, and these positions may change without notice. No guarantees are made regarding the continuation of these positions.

Forward-looking statements, estimates, or forecasts provided are inherently uncertain and based on assumptions that may not occur. Other unforeseen factors may arise that could materially affect the actual outcomes or performance of the securities discussed. BeanWealth has no obligation to update or correct any information after the date of publication.

BeanWealth disclaims any liability for losses or damages, whether direct or indirect, resulting from the use of the information provided. By accessing or using any BeanWealth content, you agree to this disclaimer and our terms of service.

Unauthorized distribution, reproduction, or sharing of this content is strictly prohibited and subject to legal action.